Speech given by Ferdinand Lips at the University of St. Gallen on 24 June 2004 as part of the International Finance & Security lecture series.

I would like to thank the organizers, Mr. Graf and Mr. Brunner, for inviting me here today. It says a lot that you have chosen such a contentious topic as gold. That shows courage. Indeed, until recently it was almost taboo to mention the word gold. Anyone who did so risked being labeled eccentric. But you were quite right in choosing this topic. You will soon see the extent to which gold has played a central and positive role in human history since the dawn of civilization.

I will provide evidence that without a gold-backed currency we are destined to face crises and military conflicts throughout the world. The best proof of this is provided by the events of the 20th century and the dawning 21st century.

I will also prove, or at least assert, that without a new gold standard the world will descend into a new dark age. I don’t know what the significance is, but the calendar of the ancient Mayan civilization ends in the year 2012. In my estimation, the current financial system, or non-system as I call it, will no longer exist by that time. As you know, it is based on deception and a mammoth debt burden that can barely be serviced anymore. In all likelihood, this mountain of debt will overwhelm the world someday.

I also want to give you hope, however, by describing to you how once upon a time there were better financial systems than the one we have today. My speech is also an appeal to you. I appeal to you young people to think of gold as money. Engage in monetary archeology. Try to devote some thought to the gold standard. It is up to you to save the world. No one will do it for you.

Today’s situation stems from abandonment of the gold standard

All of the bad things happening in the world today can be traced back to two specific events. They have given rise to the most troubling issues of the 20th century and now of the 21st century, including political dilemmas, wars, monetary crises, economic emergencies, widespread poverty, racism, the Holocaust, mass migration and terrorism. All of these things are overwhelmingly attributable to these two developments.

The first event is the abandonment of the gold standard at the beginning of World War One in 1914, and the second event is the establishment of the Federal Reserve System in the USA in 1913. World history demonstrates that there is a close relationship between monetary systems and war and peace.

And economic history shows that financial markets only function smoothly under a gold standard.

It is also evident that there is a close relationship between monetary systems and ethics and morality.

Unfortunately, it is not widely known that the 19th century was a period of prosperity and economic growth without inflation.

It seems like a fairytale when we discover that in those days the world’s major currencies remained stable over a long period. The French franc, for example, remained solid for 100 years. It was the age of the gold standard.

The lifespan of currencies (2):

|

French franc |

1814–1914 |

100 years |

|

Dutch guilder |

1816–1914 |

98 years |

|

Pound sterling |

1821–1914 |

93 years |

|

Swiss franc |

1850–1936 |

86 years |

|

Belgian franc |

1832–1914 |

82 years |

|

Swedish krona |

1873–1931 |

58 years |

|

German mark |

1875–1914 |

39 years |

|

Italian lira |

1883–1914 |

31 years |

Source: Pick’s Currency Yearbook 1977–1979

How the gold standard worked

The basic rule of the gold standard was a fixed price for gold, i.e. each currency was convertible into gold at a specified rate. The currencies were backed by gold and redeemable in gold on demand. A nation’s monetary reserves consisted of only gold. On an international level, importing and exporting gold was unrestricted. All balance of payments deficits were settled in gold. (Balance of payments: the sum of all transactions between the domestic economy and the rest of the world.) Gold thus had a disciplining influence on a national economy.

It limited public spending. It provided citizens a currency that maintained its value and was internationally recognized. In such a system, if a balance of payments deficit develops because domestic prices go up, gold automatically flows out of the country. This leaves less gold available for internal money circulation, and prices will thus come under control or decline. Exports become competitive again, and the balance of payments reverses. If, on the other hand, a country has a balance of payments surplus, gold will flow in and allow the economy to expand. Upward revaluations or devaluations were unthinkable. The system maintained it stability automatically. This is one reason why politicians do not like gold. Gold forces them to balance their budget.

Stable currencies through the ages

History offers many examples of monarchs and kings who exercised great discipline in creating money. Ancient Greece, where the first gold coins were minted, provides one such example. Due to its gold content, the drachma in effect became the global currency of the civilized world at the time. During this period, the Greek cities thrived. And economic trade flourished.

The most impressive example of a nation with healthy money was Byzantium. In keeping with the ancient tradition of stable money in Greece, Emperor Constantine decreed the creation of a new coin named the solidus. For over 800 years, the solidus served as a global currency, circulating from China to the British Isles and from the Baltic Sea to Ethiopia.

Byzantine laws regarding monetary matters were very strict. Before someone was accepted into the bankers’ guild, the candidate needed sponsors. These people had to provide a character reference. The authorities wanted to be certain that the candidate would never counterfeit money. Anyone who violated these rules had their hand cut off.

It is an amazing historical fact that the Byzantine Empire flourished as the center of global trade for 800 years. During this period, there was not a single devaluation or any amassing of debts. Neither in antiquity nor in modern times has anyone else set such an example. Through its money, Byzantium controlled both the civilized and uncivilized world at the time. This outstanding phenomenon came to an end when Emperor Alexius Comnenus, who had high gambling debts, was forced to devalue. The Turks marched in 200 years later, and the splendor was over.

Another outstanding example of the success of standardized gold coins was the gold dinar of the Arabian Empire. At its peak, this empire extended from Bagdad to Barcelona. The rise of the Italian city-states like Florence, Siena, Venice and Genoa was only made possible thanks to a new gold currency, the Florentine fiorino d’oro. A stable, reliable gold currency spurred an upswing in trade and promoted prosperity in the Italian city-states and broad areas of Western Europe. Gold as money formed the economic basis of the Renaissance. Cultures thrive only when prosperity prevails, not when people are poverty stricken. The power and the natural reliability of gold, in turn, brought mankind to a higher level of civilization.

In their great wisdom, the founding fathers of the USA stated in the American constitution that only gold and silver should be considered legal tender. The concept of paper money and a central bank were a horror for them. Today, all of this is ignored and viewed as anachronistic.

The 19th century gold standard, the highest monetary achievement of the civilized world

The gold standard was neither conceived at a monetary conference nor the brainchild of some genius. It was the result of centuries of experience. Great Britain was the architect. At the height of the gold standard at the beginning of the 20th century, there were about 50 countries, all of them leading industrialized nations, which participated in the gold standard. It was one big clearance community, and it worked.

In his book Währungen am Scheideweg (3) (Managed Money at the Crossroads – The European Experience), Professor Melchior Palyi wrote in 1960:

“For the first time since Rome’s prime did the civilized world succeed in creating a monetary unit. The commercial and financial integration of the world was achieved without the help of a military empire or a dreamy utopia. In theory and in reality, this monetary unit was accepted and recognized as the only rational currency system. Due to the automatic mechanism and the discipline to which the monetary institutions were tied, fluctuations in the exchange rates were very limited if not altogether impossible. This was the incalculable advantage of a gold currency.

Capital could be used for short-term as well as long-term transactions. Trade and industry were able to plan ahead. Especially the automatic mechanism and the rules of decent behavior in monetary affairs observed at the time liberated the value of money from the impact of governments’ whims. They substantially stabilized it on a worldwide basis. Despite all assurances by the monetary reformers, no reasonably equivalent replacement has been found in the meantime.”

Economist Ludwig von Mises wrote in his book Human Action (4):

“The gold standard was the world standard of the age of capitalism, increasing welfare, liberty and democracy, both political and economic. In the eyes of the free traders its main eminence was precisely the fact that it was an international standard as required by international trade and the transactions of the international money and capital market. It was the medium of exchange by means of which Western industrialism and Western capital had borne Western civilization into the remotest parts of the earth’s surface… and creating riches unheard of before. It accompanied the triumphal unprecedented progress of Western liberalism ready to unite all nations into a community of free nations peacefully cooperating with one another... The gold standard is certainly not a perfect or ideal standard. There is no such thing as perfection in human things. But nobody is in a position to tell us how something more satisfactory could be put in place of the gold standard.”

Before Alan Greenspan (5) (6) sold his soul, he described the gold standard as promoting prosperity and freedom.

According to him at the time, only this monetary system could prevent the chronic deficit spending of the welfare state and the recurrent speculative excesses of the financial world that result in depressions. He believed that gold and economic freedom are inseparable, that the gold standard is an instrument of laissez-faire and that each implies and requires the other. A true division of labor economy cannot exist without gold.

The era of the gold standard during the 19th century was the golden age of the white man, as well as Japan. During this period, after Napoleon, there were only seven wars of any consequence.

Post-Napoleonic wars in the 19th century

|

1855 |

Crimean War |

|

1861–65 |

American Civil War |

|

1866 |

Austro-Prussian War, North German Confederation |

|

1870–71 |

Franco-German War |

|

1877–78 |

Russian-Turkish War, Congress of Berlin |

|

1894–95 |

Sino-Japanese War |

|

1900 |

Anglo-Boer War in South Africa |

And furthermore: There was no terrorism of the scope we know today.

Assertion

I assert that if the gold standard had been maintained and if the warring nations had kept on observing the rules of the gold standard, World War One would not have lasted very long at all. Because of the automated mechanism and the prevailing rules of decent behavior at the time, financing the war on credit in a Keynesian fashion would not have been possible. (Parenthetically, Swiss historian Jacob Burckhardt describes Keynes as one of the great destructive forces in world history, along with Karl Marx.) Soon after the onset of World War One, the moment came when the world turned to monetary fraud. Political pressure to finance the war by issuing bonds made it impossible to pursue a sane monetary policy and drove the currencies to ruin. Without deficit financing, the war would have lasted for 6 months at the most. But without the discipline of a gold-backed currency, it went on for 4 1/2 years. The world lay in ruins, and millions of young people, indeed an entire generation, were lost on the battlefields.

The demise of the gold standard topples the old world order

The catastrophe of World War One also signified the passing of the old world order. Stefan Zweig’s book Die Welt von Gestern (7) (The World of Yesterday) describes how comfortable the world was before the war. Financing the war had a particularly ruinous effect on Germany, the country with the most robust and thriving economy at the time. The Reichsbank financed a large part of the war expenditures on a short-term basis, i.e. not with long-term War Loans like the British. This fact, in addition to the Treaty of Versailles and unreasonable reparation payments, led to hyperinflation, to the destruction of the middle class and, finally, to Hitler. It thus set the stage for World War Two. Look at what the shortsighted socialists have made out of the economic miracle with their welfare state: a lamentable Germany.

The monetary tragedy of the 20th century

The return to the gold standard after World War One was a fait accompli. But it lacked wisdom and conviction on the part of those in charge. At the Conference of Genova in 1922, the gold exchange standard was introduced.

Please note that it was not the gold standard that was reestablished, but rather the watered-down gold exchange standard that was launched. This meant that, apart from gold, the central banks could also dollars and pounds (i.e. the currencies of the triumphant nations) as reserves. Suddenly, dollars and pounds were equivalent to gold. That was inflationary because dollars and pounds were now accounted for twice: first in the country where they were issued, and second in the country that held them in reserve.

Furthermore, it should have been obvious that these paper currencies were in no way immune to losses in purchasing power. Therefore, they could not be lasting and generally valid yardsticks. Gold always retains its value – paper currencies do not. One of the most catastrophic decisions in monetary history also occurred when despite the emergence of inflation in the meantime, Winston Churchill, as Britain’s Chancellor of the Exchequer, chose to maintain the gold parity at the same level as it had been in 1914 instead of devaluing the pound. The Fed, facing a mild economic downturn in the USA in 1927, began providing large amounts of liquidity to the banking system. Moreover, it wanted to help out the Bank of England, which was losing a lot of money at the time because fixed income investments in the USA were more attractive. In order to lower the interest rate level, the Fed thus pumped even further liquidity into the system. This money eventually made its way to the equity markets, and the situation got out of hand in 1929. When the authorities decided it was time to stop the boom, it was already too late. The USA’s economy collapsed and dragged the world into the Great Depression of the 1930s. To this very day, the proponents of planned economies blame the gold standard for this debacle. But there was no gold standard anymore. If there had been, it would have worked at the time.

Central banks, banks and wars

When the gold standard was abandoned, central banks were the last barrier to rampant money creation, as long as they were able to maintain their independence. In the meantime, however, we have learned from bitter experience just how ineffective these so-called keepers of stability have been. Central bank independence did not turn out how it was intended to be. Central banks became compliant pawns of the governments. Indeed, it is precisely the central banks and the banking system that, through their creation of credit, have made deficit spending and war expenditures possible, and even promoted them in many instances. In his book Debt and Delusion (8), British economist Peter Warburton places most of the blame for the deterioration of economic and financial policy since the early 1980s on the central banks. There are no golden brakes anymore.

The Federal Reserve System

The most ominous and threatening event in central bank history was the establishment of the Federal Reserve System in the USA in 1913. The Bank of England and Germany’s Reichsbank served as a model. If you do not appreciate at the moment why I view the foundation of the Fed as ominous, I advise you to read the book The Creature from Jekyll Island – A Second Look at the Federal Reserve System by G. Edward Griffin9). Under the pretext of protecting the public against bank crashes and maintaining a stable value of money, the US Fed (which is not federal at all, but rather very private) is a cartel that is designed to protect its members against unwelcome competition and, in the event of losses, to pass these on to taxpayers. Its foundation flies in the face of the American Constitution envisioned by the founding fathers. Presidents like Thomas Jefferson and Andrew Jackson were always against the establishment of a central bank. It came into being in a very devious manner, as the Federal Reserve Act was pushed through Congress just prior to Christmas of 1913, when most delegates were already at home with their families. Its foundation violates the American Constitution, which states that only gold and silver should be considered legal tender.

Mr. Griffin recommends abolishing the Federal Reserve System for the following reasons:

1. The Fed is incapable of achieving the goals it has set for itself, namely maintaining a stable value of money. Since its foundation, the value of the dollar has fallen by more than 95%.

2. It is a cartel that violates the public interest.

3. It is an outstanding instrument for promoting exorbitant pricing by the banking system.

4. It creates highly unfair taxation.

5. It encourages and abets wars.

6. It destabilizes the economy.

7. It is an instrument of Totalitarianism.

The state, or more precisely, the welfare state

Economist Wilhelm Röpke, one of the men behind Germany's economic miracle (10), once said: “One can venture the claim that governments very rarely had complete control over their currency without abusing it. In today’s age of the welfare state, the probability of such abuse is greater than ever before.”

Today the gold standard is needed more than ever, for we all know from bitter experience that politicians cannot be trusted. The current political establishment will therefore stubbornly resist any attempt to introduce a gold-backed currency because such a currency would make it impossible to maintain today’s welfare state. The welfare state’s existence is predicated on government deceit of the citizens since it bears the most responsibility for the eroding value of money.

The unfortunate decisions made at Bretton Woods in 1944

The world had not learned anything at all. At the end of World War Two, it was decided to introduce the gold-dollar standard. The USA was thus granted the appalling monopoly to settle its debts with paper money it printed itself, which Charles de Gaulle referred to as the exorbitant privilege. Nobody could have resisted such temptation. A direct result of this was the inflation of the 1970s.

I ask you to consider the fine points: After World War One, we went from the gold standard to the gold exchange standard with dollars and pounds. Then after World War Two, we then proceeded to the gold-dollar standard. The pound had lost its previous stature in the interim and was no longer suitable as a reserve currency. As a sign of the USA’s growing economic power, apart from gold the dollar remained the world’s only valid reserve currency.

When President Nixon unilaterally abandoned this arrangement on 15 August 1971, it was tantamount to the bankruptcy of the USA. The era of floating exchange rates began in 1973. That fully opened the floodgates for money creation, credit expansion, deficit spending and speculation. As far as the ominous foundings of the IMF and the World Bank are concerned, we don’t have time to discuss them in depth today. Suffice it to say that there is no doubt that both institutions encouraged and supported Socialism around the world.

Today’s international order as a consequence

In a speech on 7 August 2002, President George W. Bush said the following: “There is no telling how many wars it will take to secure freedom in the homeland.” With this comment, Mr. Bush announced that there might not only be a war against Iraq, but many wars around the globe. He did not define when a war would be considered won or lost. This means these wars may continue indefinitely. Once again, they will be financed by deficit spending and through the banking system. This would not be possible under a gold standard.

I will now take a closer look at how the USA will be able to pay for these wars. In principle, the USA is bankrupt. The trade balance deficit is approaching 600 billion dollars, the budget deficit exceeds 500 billion dollars, and its foreign debt is enormous.

The USA has indeed already been bankrupt since 15 August 1971. That was the day America escalated its war on gold. Not unlike a banana republic, the USA defaulted on its obligation to redeem dollars for gold. If you are bankrupt, you theoretically should not be able to wage any wars. Under the discipline of the gold standard, it certainly would not be possible. Despite this, however, the USA can wage war and simply pay for it with its unbacked paper money, with fake money so to speak.

Who, then, actually pays for these wars? The answer is simple: We all do! It was the same in the case of Kennedy’s and Johnson’s Vietnam War. The world helps to finance the deficits, and the Americans wage the wars. That is ultimately the disgraceful result of abandoning the gold standard. But nobody notices, or is willing to admit it. That’s how it is: We are all partly to blame.

The 20th century and the onset of the 21st century

Contrary to the 19th century – with its solid and inflation-free growth, notable currency stability and relatively small number of wars – the 20th century was marked by inflation, hyperinflation, currency and trade wars, waves of speculation and military conflicts. The 20th century also brought two world wars, hundreds if not thousands of local wars, hundreds of millions of casualties, wholesale genocide, mass migration, worldwide monetary erosion, economic ruin, gigantic slums, the Aids epidemic and, ultimately, the decline of civilization.

Why are there wars?

Among the various motivations for international disputes that have ultimately led to war, economic reasons have undoubtedly been the most significant – from the primeval struggles for hunting territories, pastures, salt mines and fertile valleys, to the predatory attacks and conquests of the seafaring and trading nations, all the way to modern battles for living space, sales territories and, the most important motivation of all, access to natural resources. However, domestic political problems have also played a large role. Wars have frequently been started to divert attention from problems on the home front.

In the Middle East, both aspects have been important to the Americans, namely:

Control over the oil resources of the Middle East

Distraction from the disastrous condition of the US financial system

Saddam Hussein was only a pretext. Let’s not forget that the USA had previously built him up and supported him as a buffer against Iran.

There is one more reason, however, and that is the unbelievable arrogance of the US government. But now the arrogant leaders in the USA are feeling the backlash. First this is a war that can’t be won, and second it is doing even more damage to the dollar. Wars have always undermined the purchasing power of currencies. Whereas a gold coin from the time of Alexander the Great still shines as it did then, paper currencies are destined to revert eventually to their intrinsic value, and that is nil.

The Germans know a thing or two about that. They suffered a total loss after World War One, another total loss after World War Two, and were ultimately admitted to the European Monetary Union, thus accepting the euro as their currency. And this all happened in less than a century.

Gold is freedom

Not only is there a correlation between gold-backed currencies and war, but also between gold-backed currencies and freedom. In a famous essay entitled Gold and Economic Freedom (5) that current US Fed Chairman Alan Greenspan wrote in 1966, he said the gold standard promotes prosperity and freedom. When we recall that one of the first official acts of Lenin, Mussolini and Hitler (and, by the way, Franklin D. Roosevelt) was to forbid the private ownership of gold, this relationship becomes clear. Even now, the price of gold is still manipulated each day and kept artificially low. Those in power want to maintain the fictitious status of the dollar, at least for as long as possible. In my book Gold Wars (11), I described this manipulation.

Why is gold being manipulated?

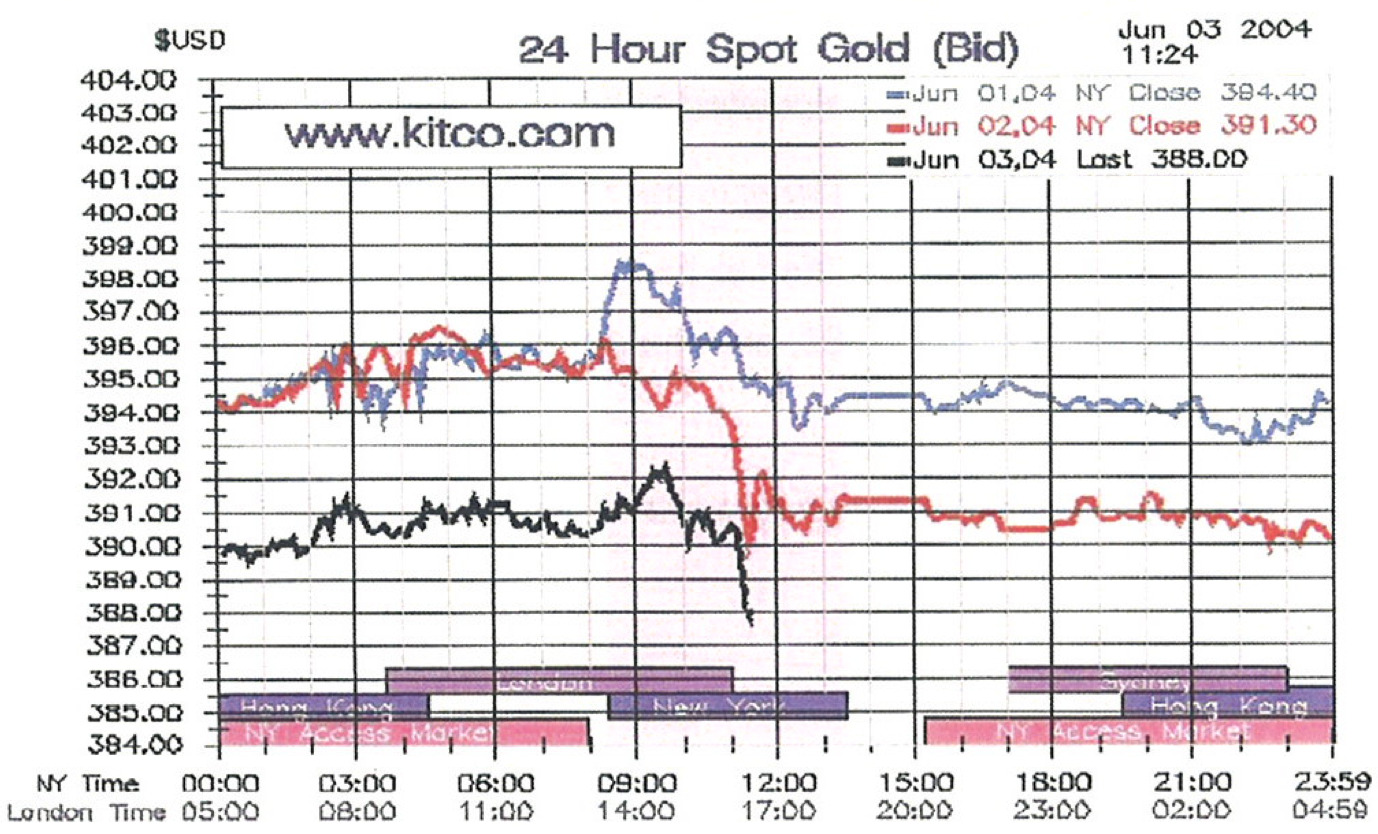

Gold is indeed being manipulated each day by a clique of reckless financial wrongdoers. The following chart shows the gold price movements and manipulation over a one-day period. You can clearly see what is happening here.

Normally, the price of gold rises in Europe, but as soon as the COMEX opens in New York it is driven downward – more on some days, less on others. And this takes place without regard to the harm, and by that I mean the economic damage, that it causes throughout the world.

Why are these financial wrongdoers interested in manipulating gold?

In each and every discussion about the future of gold and its price, one thing needs to be clearly understood:

GOLD IS A POLITICAL METAL.

And this is so for the simple reason that given its historical role as money, gold just isn’t compatible with the modern financial system. Up to 15 August 1971, there was never a period in history during which no currency was linked to gold.

The world’s history of currencies is full of examples of devaluations, coin clipping and bankruptcies. Yet it was always possible to switch to other currencies that were backed by gold. But if you disregard the Swiss franc, this has no longer been possible since 1971.

All of the economic, monetary and financial catastrophes of the past 30 years can be traced back to this event.

Today’s system of unbacked paper money is still very young. It relies solely on faith – faith that the debts upon which it is based will be repaid someday.

A single, one-off event that could shake this faith, and thus the foundation of the financial system, is a robust upsurge in the dollar price of gold.

That is the entire reason why gold is manipulated each day.

But we know from the history of the Gold Pool in the 1960s that gold cannot be manipulated endlessly. At the time, the central banks tried to fix the price of gold at 35 dollars an ounce. The Gold Pool fell apart on 17 March 1968, and the entire pitiful experiment became the object of ridicule.

Gold is very cheap today because the governments of the world tamper with its price on a daily basis.

Where do we stand today? In a world at war and in crisis

1. We are in the midst of a global currency and devaluation war.

2. The world’s reserve currency, the dollar, is weak because of the USA’s alarming financial situation – more than 34 trillion dollars of debt, 200 trillion dollars of derivatives and some 10 trillion dollars of obligations outside of the official government accounting. (And just think, in 1997 there were fears that the global financial structure would collapse due to a single hedge fund, Long Term Capital Management, with total assets of 3 billion dollars.)

3. The money supply is increasing dramatically in the USA and worldwide.

4. The stock markets currently resemble casinos; they are overvalued and dangerous. The Dow Jones Index is manipulated each day by the Working Group on Financial Markets (established in 1987 by President Ronald Reagan). There are no free markets anymore. The insiders are getting out.

5. We face negative interest rates (i.e. inflation exceeds interest income), which are bad for investment and the economy.

6. There is a deficit between gold production and demand – central banks have loaned out 1/3 to 1/2 of their gold. The gold is gone. Panic could ensue if people realize that gold is the only safeguard of monetary value and that a large portion of the central banks’ gold has been sold.

7. The mountainous debt has reached historically high levels worldwide. This will place an onerous interest burden on the young generation and may be impossible to finance. It could result in panic or might be dealt with through inflation.

8. The current erosion of money is catastrophic for wage earners and retirees. The Middle Class is being squeezed. A billion people around the world live in poverty stricken areas. Soon, one out of every three city dwellers will live in slums. Such conditions will promote the spread of radicalism. Hate is growing.

9. The global economy will be in a Kondratieff winter over the next 10 years. Humanity has managed to overcome every crisis up to now, but given the current means of monetary degradation, it will not get through this crisis without serious consequences.

10. Political confusion is on the rise. The geopolitical situation has never been so bad. A coup in the Kingdom of Saudi Arabia could, by itself, have a disastrous impact on the flow of oil and the global economy.

At this point, allow me to provide a quote from a speech given in Washington D.C. in 1948 by Congressman Howard Buffett, father of the most successful investor of all times, Warren Buffett:

“Because of our economic strength, the paper money disease here may take many years to run its course. But we can be approaching the critical stage. When that day arrives, our political rulers will probably find that foreign war and ruthless regimentation is the cunning alternative to domestic strife. That was the way out for the paper-money economy of Hitler and others... For if human liberty is to survive in America, we must win the battle to restore honest money. There is no more important challenge facing us than this issue – the restoration of your freedom to secure gold in exchange for the fruits of your labors.”

Ladies and Gentlemen, these are the subtle relationships between freedom, money, intellect, war, peace and gold.

Ladies and Gentlemen, I believe I have now provided sufficient reasons for the necessity of a healthy, stable currency based on gold. It is the only solution! We must go back to honest money, back to the gold standard.

Or as Otto von Habsburg (12) once said: “Ethics and morality are still the safest approach to take in all fields".

In conclusion, I will therefore allow two other gentlemen with a renowned grasp of world affairs to speak out on the topic of a gold-backed currency.

The internationally recognized investment consultant Harry Schultz has given us one of the best definitions of the gold standard: Standards (gold and other) (13):

"I have written several times in the last 36 years and I want to restate this principle with force: I am pro-gold regardless of the price! I don’t fight for gold in order to make a profit on gold shares, bars or coins! Gold is important for far more important reasons and I would be embarrassed to promote gold only for monetary gain. Gold is the essential linchpin for our individual (not group or nation) freedom. Gold belongs to the monetary system as a governing factor. We belong back on the gold standard. I used to compromise and say a quasi-gold standard will probably do, a modified Bretton Woods version. And that may be what will evolve, but in my view we should fight for a pure gold standard, the old-fashioned form, because it worked! And not just for fiscal reasons! It forced nations to limit their debt, spending and socialist schemes, which meant sound behavioral habits were formed around those limitations, and those habits rubbed off on everyone. People were more honest, moral, decent, kind, because the system was honest and moral. Cause and effect. Today we have cause and effect of the opposite standard: no limits on what governments can do, control, dictate; no limit on government debt, welfare or socialist schemes. There is no governor on the government.

This habit rubbed off on the public, causing them to go into debt, lose respect for the system and morality. The effect brings us more divorce, fraud, crime, illegitimate births, broken homes. When the money of any country loses its base/backing there is no standard for any behavior. Money sets a standard that spreads into every area of human activity. No paper money backing, no morality. That is why gold coin money worked so well and why the US moved into paper money very slowly, carefully, keeping the paper dollars backed 100% by gold. But slowly, like slicing a sausage, that backing was removed in stages, ‘til now there is none. The effect of this cause is all around us. Violent films reflect violent society reflect no respect throughout society. Layer by layer, we are corrupted when money loses certainty. Today’s stock market bubble is part of the scene as will be tomorrow’s mega-crash and mega-recession. Big Brother was made possible through the absence of automatic controls and loss of individual freedom via non-convertible currency. So, pass the word. Fight for gold. Not for profits, though they are helpful and help us fight for individual freedom, but for a future that returns to sanity in various standards. If we have a gold standard we get a golden human standard! The two are intertwined. They are the ultimate cause and effect. Gold blesses.”

Charles de Gaulle, President of France, gave his country the greatest gift he could offer: He restored France’s confidence.

On 4 February 1965, he said::

“The time has come to establish the international monetary system on an unquestionable basis that does not bear the stamp of any country in particular. On what basis? Truly, it is hard to imagine that it could be any other standard than gold. Yes, gold whose nature does not alter, which may be formed equally into lingots, bars or coins; which has no nationality and which has, eternally and universally, been regarded as the unalterable currency par excellence.”

Bibliography:

(1) Lips, Ferdinand, Die Gold-Verschwörung, Rotenburg, Ed. Kopp, 2003

(2) Lips, Ferdinand, Das Buch der Geldanlage, Dusseldorf, Ed. Econ, 1981

(3) Palyi, Melchior, Währungen am Scheideweg, Francfort-sur-le-Main, Ed. Fritz Knapp, 1960

(4) Mises, Ludwig von, Human Action, New Haven, CT: Yale University Press, 1949

(5) Greenspan, Alan, «Gold and Economic Freedom», dans Capitalism: The Unknown Ideal, Ayn Rand éd., New York, NY: New American Library, 1967

(6) Parks, Lawrence, What does Mr. Greenspan Really Think? New-York: Foundation for the Advancement of Monetary Education FAME, 2001

(7) Zweig, Stefan, Die Welt von Gestern, Stockholm: Ed. Bermann-Fischer, 1944

(8) Warburton, Peter, Debt and Delusion, Middlesex, Angleterre: Alan Lane The Penguin Press, 1999

(9) Griffin, G. Edward, The Creature from Jekyll Island – A Second Look at the Federal Reserve System: Westlake Village, Californie, American Media, 1994

(10) Röpke, Wilhelm, Jenseits von Angebot und Nachfrage, Erlenbach/Zurich, Ed. Eugen Rentsch, 1961

(11) Lips, Ferdinand, Gold Wars – The Battle Against Sound Money as Seen From a Swiss Perspective, New-York, NY, Foundation for the Advancement of Monetary Education FAME, 2002

(12) Habsburg, Otto von, Ethik und Moral des Geldes, Frankfurter Allgemeine Zeitung, supplément «Geist und Geld» du 18 avril 1988

(13) Lips, Ferdinand, Die Gold-Verschwörung, Rottenburg, Ed. Kopp, 2003

(14) Rueff, Jacques, New-York, NY, Macmillan,1972

Original source: Lips-institute

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.